Intermodal transport performed well, with a 27% increase in traffic year-on-year

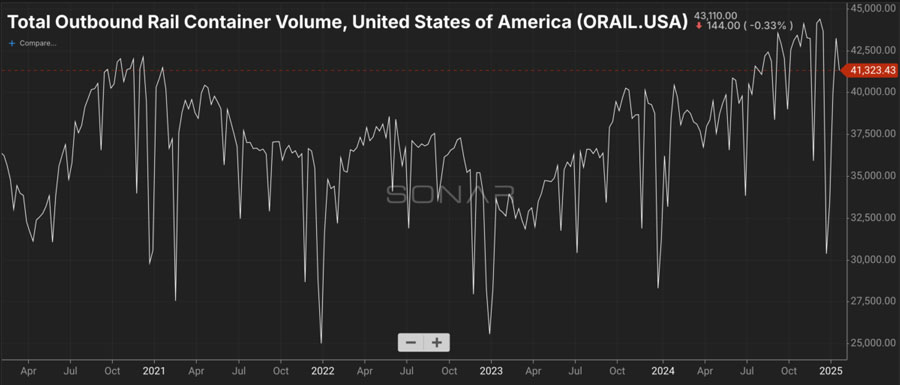

The intermodal rail market soared in the third week of January, with volumes up 27 per cent year on year, helped by easier year-on-year comparisons during a typically weak seasonal period. That weakness has not materialed this year, as intershipment growth continues to be driven by high Chinese exports, a strong U.S. consumer and shippers' stockpiling in response to tariffs.

Leading the way among the major railroads, CPKC saw a staggering 38% year-over-year increase in volume in the third week, Union Pacific saw 36% year-over-year volume growth, and Canadian National saw 31% year-over-year volume growth. BNSF's interconnect was up 29% year-over-year in Week 3, CSX's was up 28% year-over-year, and Norfolk Southern's was up 20% year-over-year.

Container traffic appears to have peaked, but remains super-seasonal and strong compared to the same period last year. In January, sea container traffic into the United States recovered well and maintained strong growth for a longer period, but still peaked in August 2024. Intermodal traffic appears to be following the same trend, but with a delay of several months.

Despite increasing ridership, rail companies have responded to this growth by strategically maintaining staffing levels. The four largest U.S. railroads - BNSF, CSX, Norfolk Southern (NSC) and Union Pacific (UNP) - worked together to keep their headcount relatively flat, with total headcount down about 2 percent year over year. This approach was largely due to job cuts at CSX (-0.3%) and BNSF (-0.7%), offset by marginal increases at NSC (+ 0.3%) and UP (+ 0.1%).

The rationale behind this strategy is to improve operational efficiency and productivity. By taking advantage of technological advances and optimizing processes, rail companies aim to handle the growing volume of intermodal traffic without a corresponding increase in the number of employees. Union Pacific CEO Jim Vena, for example, highlighted productivity gains at an investor conference in December that have allowed the railroad to manage stable volumes with fewer employees. Similarly, CSX is forecasting a flat headcount in 2025, anticipating that its existing workforce can absorb increased demand through efficiency measures.

Despite the positive outlook, the railway company is aware of potential risks that could affect its ambitious growth targets. Factors such as capacity constraints on the rail network or fluctuations in freight prices may pose challenges. However, the proactive measures taken to optimize headcount and improve operational efficiency provide a buffer against these uncertainties, enabling railway companies to respond effectively to potential headwinds.

Diversified growth in commodity types may protect railroads from a recession as much as anything else: Grain shipments on Tier 1 railroads have risen 15 percent so far this year, petroleum product shipments have risen 10 percent, and chemical shipments have risen 7 percent.

The resilience of the intermodal market in the third week of January 2025 (usually a trough in rail traffic) is a very different signal from the typical noise. While intermodal rail competes with trucking for the longest haul distances, it is the backstop of truck volumes for shorter haul distances, often indicative of shippers' attitude towards their inventory. Looking ahead, the question is how deep a seasonal trough, if any, intermodal volumes will experience this winter before they begin to regain momentum toward the traditional late fall peak.